Most websites you bump into when you browse for financial freedom for seniors are from either financial institutions or care organizations. This article focuses on the fundamental you will have to build, if you want to work towards financial freedom.

Financial freedom is defined as having enough income to pay for living expenses for the rest of your life without being employed or dependent on others.

You will achieve that when you retire or receive a large inheritance. But also if you find a way to get paid for your work more than once.

Writers and musicians receive royalties on their book or piece of music. Computer programs and apps are sold. Examples of creating something once and getting paid as often as something is sold.

Table of contents

What will financial freedom mean for you?

You have looked for ways to become financially free and you are either a senior or well on your way to becoming one, otherwise you wouldn’t have wind up on this website. But some answers you won’t find because you can only formulate them yourself.

Like answers to these questions:

- What are beliefs and messages I have about money?

- Why can’t I have money?

- Why am I afraid of being wealthy?

- I think rich people are . . .

Related: A Lottery to make Money? How to become Financially Healthy

Does financial freedom mean you are rich? And if so exactly how rich do you want to be? You need to know your numbers to answer this question. Making it necessary to build on the fundamentals.

If you want to achieve financial security, you’ll want to pay attention to your banking habits. There are a lot of healthy banking habits you can develop to improve your financial situation and generate security for the future.

Here are some of the best banking habits that support financial security.

Best banking habits

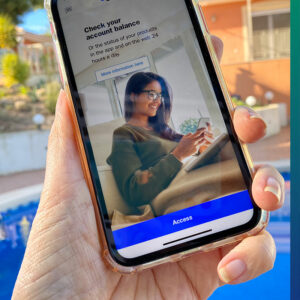

Regularly check your banking app

Technology has made it possible to keep an eye on our banking accounts. Most banks have their own apps which allow you to check your balance, as well as transfer money and make payments through your phone or tablet device.

By frequently checking your banking app, you’ll be able to track your spending. It also enables you to identify any potential issues early on. While you don’t want to think about it, there is always the risk of fraud. Getting money back after it’s been wrongly taken from your account isn’t always easy, unless you do something about it right away.

So, start checking your banking app daily to monitor your spending, and watch out for suspicious activity.

Cut back your spending

Achieving financial security isn’t easy in today’s economy. However, by making small cutbacks in your spending, it can really help. You might be surprised how much you can cut back on.

Check how much you spend on utility bills and compare the options available to see if you can make a cheaper deal. Also, look at what you spend on a weekly or even daily basis. Meals out, trips to the movies, and even those daily bars of chocolate all add up.

Avoid having an overdraft

Being able to overdraft your bank account can give you great peace of mind. However, it can also cause endless problems if you don’t use it wisely. Ideally, you completely avoid an overdraft. That way, there is no chance you’ll go over your balance and have to deal with fees.

Be sure to only use an overdraft in emergencies and to replete your account as soon as you can.

Ensure direct debits are set up

One thing that’s going to impact your finances is if you miss or make late payments. So, you’ll want to ensure you have direct debits set up to ensure payments are taken automatically.

One thing to remember here is that if you do have direct debits set up and you don’t have the money to cover them, you should cancel them. Otherwise, you could be hit by fees for going over your balance. However, don’t cancel a direct debit without first telling your providers, as this too could cause issues with late payment fees.

Common money-saving mistakes

When you’re trying to save money, there are a lot of mistakes you can unknowingly make which could hinder your progress. It’s hard enough to save money, especially if you’re on a low working income or pension.

So, if you want to ensure you’re saving correctly and getting the most from your hard-earned cash, there’s a few things you’re going to want to avoid.

Here are some of the most common money-saving mistakes and how you can avoid them.

Not setting up automatic savings

When you plan to save money, your motivation ensures that you keep making regular payments into your account. However, after a while, it’s easy to fall into the “I’ll save double next month” trap.

There will always be reasons to put off saving. Whether it’s an unexpected bill or you want the occasional treat, you’ll always find something else to spend your savings on. It’s common to view savings as a luxury more than a necessity.

To make sure you stick to your savings plan, it’s important to set up automatic savings. That way, the savings will be taken automatically from your account before you’ve had a chance to reconsider.

Saving money instead of paying off debts

While savings are undoubtedly important, it’s more important to focus on paying off any debts you currently have. Think about it. If you’re saving money but not paying off debt, you’ll be paying extra on interest payments.

Discipline yourself to pay off your debt with a fixed amount a month. That way it is easy to continue putting that amount aside on a savings account once your debts are paid off.

Keeping savings in the same account as earnings

Do you use a separate savings account? If not, you’ll want to open one. The trouble with keeping your savings in your personal account is that you’ll be tempted to spend them.

It is a lot more difficult to keep track of savings when other money flows in and out of the account. You’ll also miss out on interest as personal accounts don’t tend to provide interest on a positive balance.

And yes, I know, interest rates are very low at the moment, but even 0,5% is more than 0%.

Impulse buying

Impulse buying is a major problem when you’re trying to save. If you tend to spend money on things you don’t necessarily need and you weren’t planning on buying, you may need to get your impulse spending under control.

Ask yourself whether you really need to make the purchase. If not, put the money you would have spent into your savings account.

If you have a problem controlling yourself, it might be a good idea to withdraw a fixed amount each week and to only pay cash. When your purse is empty you’ll have to wait until next week.

Placing yourself on a spending ban

It might seem like a good idea to place a spending ban on yourself. However, this can actually hinder your savings progress. When you feel restricted, it can tempt you into going on a spending spree – a little like when you’re trying to stick to a diet that cuts out your favorite foods. You’re going to cheat if you feel restricted.

Although pocket money or allowance might sound childish, it is a great way to keep track of your finances and to avoid overspending.

These are some of the most common savings mistakes you can make. If you want to get the most out of your savings, keeping them in a separate account and setting up automatic savings is a great idea.

Related: Poor Mindset vs Rich Mindset – How to Grow the Right Money Mindset

All discipline and no fun?

If you follow the advice above, you’ll develop better banking and saving habits. The more savvy you are with your banking, the more financial security you’re going to develop. As with any habit, you need to be disciplined in order to make them a part of your daily life. If you’ve been using bad banking and saving habits for years, it’s understandably going to take time to turn them into positive ones.

Do you have to cut all the fun out of your life? Of course not. In fact, it is very important to have fun. If you are having a good time, it’s much easier to make good strategies and to be happy. There are many ways you can have a good time without spending a lot of money.

Do you have a tip I haven’t mentioned? Tell us in the comment box below.

How about having fun and being happy, while at the same time earning money?

Join me in being an affiliate marketeer at Wealthy Affiliate.

Related article: Earn a Side Income as a Pensioner – Become an Affiliate

Another great article Hannie. I fully agree with the most common mistakes people make with money.

You are so correct that paying off debt should be your first priority.

Once that is done, continue making a payment in that same amount into your savings account.

Here in Canada, we have something called a Tax Free Savings Account (TFSA) where you can save and not be taxed on the interest(which is often slightly higher than a regular savings account) until such time as you withdraw the money.

Once that money reached a certain amount I would transfer it to an RRSP(Registered Retirement Savings Plan) where you can be invested in mutual funds that pay a higher return.

The sooner in life, you get started the better because you can really take advantage of the power of compounding.

Do you have similar investment vehicles in Europe?

Sounds like great opportunities you have over there in Canada, Rick. Thanks so much for sharing this information.

Yes, there are things like that in Europe as well, but over here we have the disadvantage that every country still wants to do everything for themselves. So for instance, the rules in the Netherlands are way different from the rules in Spain. And I am pretty sure there are different ones in France, Germany and so on. Making it nearly impossible to give general advice in that regard.

But your remark to start at a young age makes a lot of sense. A small amount that is put in a savings or investment account from age 20 will be a nice amount once that person turns 65. Like you often say: ask a financial advisor. As you know I am at times hesitant about advisors, but that is only because I think that self-education should be everyone’s priority. And once you know, an advisor can add to that knowledge or discover the possible holes in a plan.

Hannie that is a very great article!

I can relate to all of that! For years we had financial problems due to my husbands’ bankruptcy. We had debts and didn’t know how to pay our groceries: awful feelings and experiences. I tried a lot, checking the second-hand shops for clothes and things we needed. Getting myself materials from the market and making my own clothes. So there is a lot of what you can do to save money. I tried all the tips you are suggesting in your article, and it worked very well.

The difficult thing is your mindset. Coming from parents who were children in the second world war helped me learn to save money but always got in the way of having a rich mindset. I could better allow myself to have debts than to have savings. That is quite difficult to change.

How do you feel that way, Hannie? Did you have difficulties too?

Like your parents, Sylvia, mine have suffered during the war which influenced their behavior. They were always turning around their coins in their hands before they spent it, so to speak. So, yes, I learned to think small, like they did.

That hinders one’s happiness. In reality, I don’t even have a lot more money than I had years ago, but my behavior towards money changed hugely. Because I have no debts anymore, I have less to worry about.

Not to be able to pay for your groceries, however, must be a devastating feeling. I am so sorry you went through such hardship. And it surely will give a different feeling if you make your own clothes because you like doing that, or because you have to. Nevertheless, it does show you are very resilient and creative in finding solutions. I admire you for that!

Take care. 🙂